Shares of Amphenol Corp. (APH) are trading at the midpoint of their March 13 high of $93.00 and their April 24 low of $82.00 - the market appears uncertain as to which way the stock will break. In my opinion, the shares of this producer of fibre-optic cables present an excellent buying opportunity at current price levels. The company has a solid history of generating strong earnings, and the future growth rate ratios point to accelerated earnings growth. I lay out my bullish argument for the company below by reviewing some pertinent fundamental and technical aspects of the stock.

Momentum Growth Quotient

Over the last few months, I have developed a new approach for my fundamental analysis of stocks: the Momentum Growth Quotient (MGQ). The MGQ is the key metric that I use to gauge the financial health of a company and its potential future growth prospects. The MGQ is calculated using the following company financial data:

EBITDA growth trend over the last 10 years Operating Margin % Operating Margin % 5-year average Normalized free cash flow over the last 7 years Forward P/E Forward Rate of Return

The goal is to generate a single number, which summarises the relative fundamental strength and future growth prospects for a company compared to an index. For the index, I use the S&P 100 - this index provides a wide swath of companies from different industries representative of the broad US economy. I update the Momentum Growth Quotient for each company in the S&P 100 every month and then use the average quotient as my baseline to compare the relative financial strength of individual companies.

As of the end of June, the average MGQ for the S&P 100 was 10.28. So, if a company has an MGQ of 12.00, its individual future growth prospects are around 20% higher than the index. If a company has an MGQ of 8, its future growth prospects are around 20% lower than the index.

The MGQ plays a critical part when it comes to determining if I am going to go long or short a stock. Generally, I only want to go long a stock with an MGQ higher than the index, and I want to go short a stock with an MGQ lower than the index.

The MGQ for APH as of the end of June was 13.57, which implies a 32.0% higher growth rate compared to the S&P 100. This tells us that APH has strong future growth potential and is a good candidate for a long position.

Financial Snapshot

Let's dig a little deeper into the financial data to get a better feel of how the company has performed on certain fundamental metrics and what these numbers imply for future growth.

The Past

During the past 12 months, the average EBITDA per Share Growth Rate of Amphenol was 15.70% per year. During the past 3 years, the average EBITDA per Share Growth Rate was 11.50% per year. During the past 5 years, the average EBITDA per Share Growth Rate was 12.20% per year. During the past 10 years, the average EBITDA per Share Growth Rate was 12.40% per year (GuruFocus). The company has been able to generate earnings on a consistent basis over the long term and there are no warning signs that this trend will not continue into the future.

The operating margin % for APH came in at a 20.19% as of March 2018. Each dollar of revenue the company generated brought in 20.19 cents of earnings. The company's operating margin came in just above the average operating margin % of 18.20% of telecom equipment providers. In regards to net income for Q1 2018, APH was able to book Y/Y net income growth of 18.04% while the average Y/Y net income for its competitors came in at -40.16% (CSI Markets).

The Future

Knowing how a company has performed in the past is important in order to evaluate management's past record in running the business. But more important to us is how profitable the company will be in the future because we are investing going forward, not backwards. And it's the forward-looking metrics that should really get you excited about APH.

I like to use two measuring sticks to gauge the future growth potential for companies: Forward P/E and forward rate of return.

There are several ways to interpret a company's Price-to-Earnings Ratio (P/E). One approach is to look for companies that have a lower P/E compared to other companies in similar sectors - the rationale being that the lower the P/E, the more a company is being undervalued by the market, hence, the more value you are buying for every dollar invested. This makes a low-P/E stock a good value, but there is also the other side of the coin - it can also indicate that investors aren't very confident about the company's prospects.

I prefer to use Forward P/E (current stock's price over its "expected" earnings per share) to gauge a company's expected future earning power. A high Forward P/E ratio means that investors are anticipating higher growth in the future and are willing to pay more for future earnings - momentum investing is all about following the trend (perceived or real).

APH has a Forward P/E of 25.32 compared to a 17.29 Forward P/E for the S&P 100. The Forward P/E for APH is higher than that of the index, indicating that investor growth prospects for the stock are higher than that of the broader market, and investors will be willing to pay more for future growth.

The forward rate of return for a stock (created by Donald Yacktman) is one of my favourite quotients for gauging the market's expectation for future growth for a company. Yacktman defines forward rate of return as the normalized free cash flow yield plus real growth plus inflation. In simple terms, the forward rate of return can be thought of as the return that investors buying the stock today can expect from it in the future.

The forward rate of return for APH stands at 15.02%. This implies that an investor buying the stock today should expect a 15.02% return over the next 12 months. The average forward rate of return for the S&P 100 stands at 9.68%, so APH has an implied potential rate of return that is 1.55x greater than that of the index.

The risk inherent in the forward rate of return is that the calculation is reliable only if the company can grow at the same rate in the future as it did in the past. If the growth rate falters, the projected returns will not materialise. But we are willing to accept this risk as part of the difficult process of forecasting earnings and growth momentum.

Technical Snapshot

As per our ChartMasterPro Daily Trade Model, the momentum trend for APH would turn bullish with a break above $90.50. This would signal a bullish breakout above broad wedge pattern on the daily charts which began to form on March 13. I expect the shares to first rally to the $90.50, pause, and then break through to the $93.00 level over the next three months.

Today, I will buy the APH 19OCT18 85 Call Options, which will provide us with approximately 12x leverage on our long trade. Our stop-loss exit signal for the trade will be a daily close below $87.00. When trading options with leverage, a stop-loss is absolutely imperative in order to avoid oversized losses and wipe-outs.

For investors in the shares, we recommend that you hold for 3 months or $93.00, whichever comes first. For longer-term investors, I believe APH is a solid addition to any growth portfolio over the next 12 months.

The Need for Speed

There's an old adage that says that if you're going to set up a business in the desert, you would do well to sell water. Amphenol finds itself in the enviable position of "selling water in the desert," where the water is fibre optic connections and the desert is a world that has developed an insatiable thirst for faster and faster connectivity speed and capacity (ok, I think I've pushed the metaphor as far as it will go!).

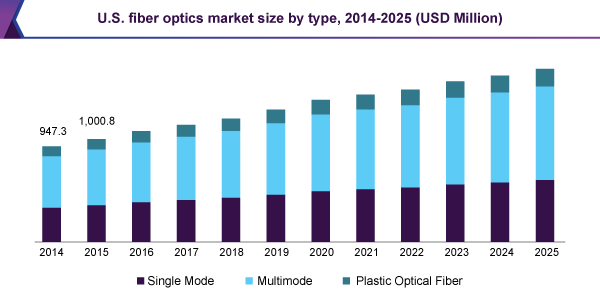

The global fibre optic market is expected to grow to $3.7 billion by 2022, which would represent a CAGR of around 5%. The chart below shows the projected growth of the US fibre optics market through to 2025 - the trend is clearly up, as demand for fibre optics products for internet, cable television, long-distance telephony, computer networking, medicine and research, and even lighting and decorating applications is expected to continue to increase domestically.

Source: Grand View Research

In its Q1 2018 earnings report, the company raised full-year 2018 guidance for both revenue and earnings. The 2018 guidance boost coupled with my robust MGQ and forward-looking growth ratios for the company are enough to convince me that shares will be moving higher in the near future.

Conclusion

When I go long a stock, I want to invest in a company that provides superior future growth potential, but I also want to time the entry into any position to try to maximise my return.

So, I use fundamental analysis to identify shares with a strong future growth rate, and then I apply technical analysis to identify ideal entry points.

In my opinion, APH is a strong buy at these levels from both a fundamental and technical perspective.

Disclosure: I am/we are long APH.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: To review the performance of my past trades, please see my blog posts.

Stitch Fix Kids.

Stitch Fix Kids.